Starting a business is a big step. It takes a plan, vision, and perseverance. It also involves business startup costs, expenses, and a lot of learning along the way. Remain flexible and put the customer first, and you’ll improve your chances of success as you locate and test demand for what it is that you have to offer the world.

Remember, it doesn’t have to be flashy or reinvent the wheel. People just have to want it and be willing to buy it.

Key Takeaways:

- Starting a business isn’t easy, but it is possible, even in today’s economy

- The more you plan ahead and research, the better data you’ll have to guide your decisions, and eventually secure outside financing if needed

- Knowing how to legally organize your business will help you to write off the majority of your initial costs in starting your business as a tax deduction, so that in 30 years, the cost to start your business might even be close to free over time

Depending on your business model, where your business operates, and your market, the average start-up costs for small businesses can vary greatly. Although there isn’t a single magic number that applies to all businesses, knowing the most typical startup costs can still guide your estimation of what your particular costs will be.

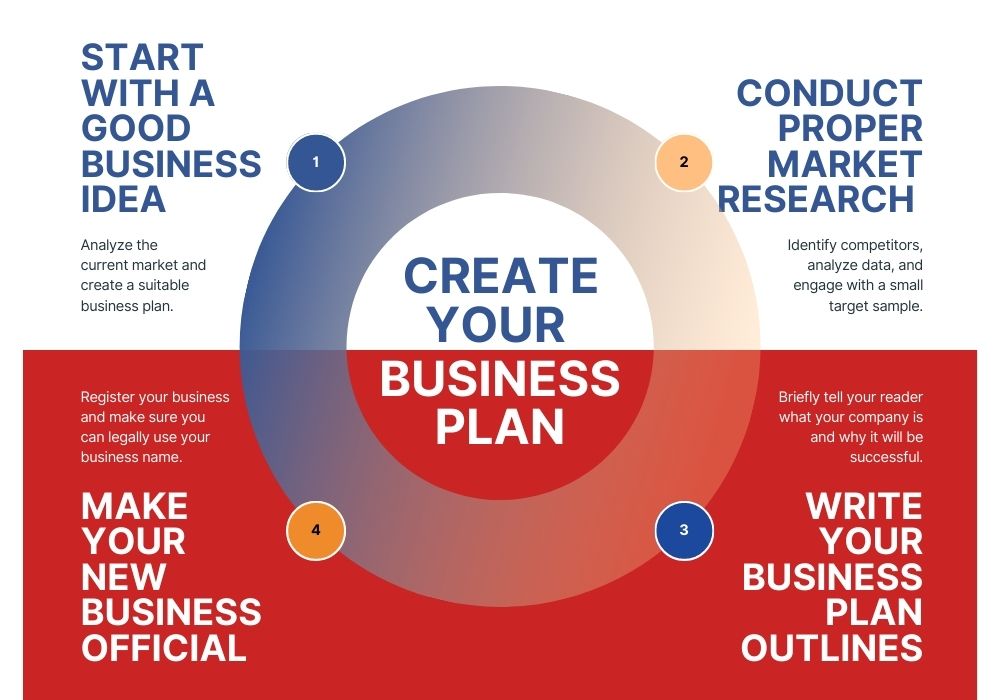

Business Startup Guide/Checklist

A physical business with a storefront or office may need to spend hundreds of thousands of dollars on a location, furnishings, and equipment, whereas an online business with no inventory may only need a couple hundred dollars for a website and marketing. Some businesses also have variable costs, such as staffing and product costs, and supply and logistical realities that change with the economy.

Here are some things you need to know about startup costs, including ongoing and one-time costs for your business.

Average Business Startup Costs

Business startup and first-year expenses can typically range between $32,000 and $42,000. However, a business can be launched with a starting investment ranging from zero dollars all the way into the millions. The sooner you can see your profit margins, the better in getting the overall picture of what starting a business will ultimately cost you, rather than going into it buying what you need as you need it until you run out of money.

However, rarely are most business owners this lucky. The reality is, many businesses may need financing. Financing is unlikely to occur without a solid business plan, and that means having as much information up front as possible. Many businesses will spend money on things they don’t need and figure out more affordable alternatives later. It’s all a part of the discovery process, no matter how you slice it.

When you estimate startup costs, you can:

- Calculate profits

- Analyze the break-even point

- Gain access to commercial loans

- Bring in investors

- Help you understand the many tax deductions that can help you save money

The Small Business Administration (SBA) offers a business startup calculator on their website to help you get some hard facts and figures. From personal experience, your strength will lie in the ability to see a market need, a profit range, and the willingness to take calculated risks.

Remember to separate personal interests from hard, provable market demand to prevent personal bias or the reasons for starting a business from preventing sound decision making.

Business Startup Challenges and Problems

Since the majority of business startups don’t make it past the 5-year point, it’s important to remember the basic premises and core concepts that will supercharge your success.

1. Determine a Real Problem to Solve

Finding a problem is the first step in starting your own business. You must offer something that people actually need or want for them to purchase from you. The only requirement is that it be something that people care about—it doesn’t have to be completely original or something that has never been done before.

In fact, that’s proof of demand, and something you can leverage to deliver superior results compared to your competition.

2. Locate Your Customers

Small businesses aren’t the only ones that struggle to find customers. Every company in the world, including Nike and Apple, needed to find customers in the beginning. Obviously, things become much simpler once you become well-known. But you can’t just wait around for customers to come in if you want your business to succeed.

You must use content to specifically target them and inform them of your company’s operations. When you first start out, this is especially crucial because you won’t have a customer base to rely on. This is also where brand awareness is important. The fact that there are so many options for customer acquisition makes this particular startup challenge even more difficult.

Where do people whom you’ll be helping with their problem live and work? What are their ages and demographics? On what platforms do they spend their time? Remember, most people use Google for looking for solutions to their problems, including the physical addresses to businesses in town. That’s just one example.

3. Brand Awareness and Growth Marketing

During the early stages of any startup, developing brand awareness is essential because it puts your name in front of your target market. Direct sales aren’t as important to many businesses as brand awareness. Customers familiarize themselves with your offering and begin to link your brand with your goods and services when they are exposed to your brand on a regular basis. This results in clients who will keep doing business with you, or consider it at a later date.

The benefit of developing a strong brand is that it attracts devoted customers who will continue to purchase your products in the future. It may seem to a startup founder like their company is lost in a sea of competing brands. With so many other companies to compete with, how can you make your voice heard and your brand recognized?

4. Effective Time Management

Despite the fact that you are “the boss,” you should not get mired in problems that you could solve by outsourcing, or that are not going to effectively contribute to the regular accomplishment of all the goals you’ve planned out to make your successful business a reality.

If you’re stubborn, you might be tempted to spend an entire afternoon on one small, insignificant thing that you just have to get perfect. Avoid this scenario, as time is one of your biggest resources, especially when you are cash-poor in the beginning.

Prioritize your time to accomplish the biggest, most impactful items now. Adjust the fine details later.

5. Choosing the Right Help (when needed)

Every successful company that scales up has a great team of employees. The more your company expands, the more employees you’ll require.

As the current economy shows, it can be difficult to find employees who meet all the requirements to do the job. Additionally, it may be tempting to hire someone on a temporary basis if you simply need to fill the position and have a backlog of work that needs to be completed.

However, if you hire the incorrect person, this could end up costing you money in the long run because you’ll have to advertise the position again. If you aren’t sure if a candidate is the right fit for the position, don’t hire them. Instead, you should be patient and wait for a strong candidate to emerge; this will happen. As time is limited and onboarding new employees takes a lot of time, you don’t want to go through the entire process over and over.

This is not something you want to do repeatedly, from integrating them into the team to teaching them how to use the software to finishing the required paperwork. You should develop ideal candidate personas for the position you are hiring for, much like you would when creating ideal customer personas. This assists you in identifying the kind of candidate you need to make sure you’ve made the right choice.

And if you can’t seem to fill a position because the employee keeps leaving or you have to fire them, you’ll need to look into other factors why it’s so difficult to get and keep someone specific to your situation.

6. Managing and Streamlining Your Business’s Workflow

Managing workflow is the next startup challenge after assembling the right team. If you don’t have the proper procedures and equipment for them to use, having the right people is useless. It’s critical that your team understands how to do their jobs and knows who to contact if they need anything, even though this will look different for every business.

Do they ask you directly or are there other people they can ask, like the office manager or a middle manager?

Small businesses are particularly affected by this because it is impossible to wear all the hats and be everywhere at once. When you attempt to assist every department with any questions they might have, you frequently find yourself being spread too thin.

You might think you should be involved in every aspect of your businesses, especially as a startup founder. Since this is your child, you should be in charge of all activities, right? But that is not only completely impossible, but also unhealthy.

As the business expands and you inevitably hire more staff, this problem will only worsen. You’ll need to learn how to delegate now because you can’t do everything yourself. And, you wouldn’t want to. Stick to what you’re good at and increase what you’re great at.

Automating workflow with project management software is a great way to keep track of things while freeing up your time.

7. Understanding and Learning Key Insights From Your Business Competitors

Knowing who your competitors are tops the list of difficulties faced by startups. You need to be aware of the other businesses you are up against because you won’t be the new kid on the block forever. These are the guys who provide a service that is comparable to yours and who are aiming for the same clientele.

You must therefore understand what they have to offer and how they are capturing market share. This helps you identify any weaknesses in your own marketing plan and may even advance yours to new heights with a different trajectory. You should gather as much information as you can about your rivals. For instance, what goods or services do they provide, how much do they charge, where are their offices located, and what channels do they use for supply, marketing, sales, and distribution?

You might be surprised to learn just how much you can (and should) reverse-engineer from your competition. A lot of success is knowing what works, then doing it better than they can somehow in a special, uniquely marketable way.

Tips for How to Structure Your Small Business

One of the benefits of starting your own business is the ability to organize income in a manner that pays yourself forward with tax deductions. This way, you lower your long-term cost and liability while maximizing your own profits.

One of the best ways to accomplish this is by incorporating. But don’t worry; it sounds harder than it actually is. And, there are many affordable business formation services out there that will do the administrative stuff for you for a small fee as well as keep you compliant on an ongoing basis.

Best/Most Popular Ways to Structure Your Business

The four most common business structures are: sole proprietorship, partnership, corporation, and S corporation. There are various pros and cons of each business entity type.

Sole Proprietor – A sole proprietorship—also referred to as a sole trader or a proprietorship—is an unincorporated business that has just one owner who pays personal income tax on profits earned from the business. Many sole proprietors do business under their own names because creating a separate business or trade name isn’t necessary.

A sole proprietorship is the easiest type of business to establish or take apart, due to a lack of government regulation. As such, these types of businesses are very popular among sole owners of businesses, individual self-contractors, and consultants. Most small businesses start as sole proprietorships and either stay that way or expand and transition to a limited liability entity or corporation.

LLC (Limited Liability Company) – A limited liability company (LLC for short) is a private limited company in the US. It is a type of business structure that can combine the limited liability of a corporation with the pass-through taxation of a partnership or sole proprietorship. According to state law, an LLC is not a corporation; rather, it is a type of company that offers its owners limited liability in many jurisdictions.

See our top picks for LLC and Registered Agent

The flexibility that LLCs give business owners is well known; depending on the situation, an LLC may choose to use corporate tax rules rather than being treated as a partnership, and, in some cases, LLCs may be organized as not-for-profit entities. An LLC is a type of hybrid business that combines elements of corporations, partnerships, and sole proprietorships (depending on how many owners there are).

Limited liability is the main trait that an LLC has in common with a corporation, and pass-through income taxation is the main trait that it shares with a partnership. An LLC is a type of business entity that can be more adaptable than a corporation and is sometimes a good choice for businesses with a single owner.

C Corporation – With good reason, the “C Corp” is the most traditional type of corporation in the United States. With the unlimited growth potential that C corporations (c corps) provide through the sale of stocks, you can draw in some very wealthy investors. A C corp is also permitted to have an unlimited number of shareholders.

In order to keep their good standing, most states require C corps to submit yearly reports and pay franchise taxes. Franchise taxes and annual reports must be filed and paid on time to avoid penalties, notices, and business closure.

C corporations are required by state law to hold annual shareholder and director meetings and to keep minutes of those meetings. Corporate minutes are used by owners and directors of a c corp to document management changes and significant corporate activities.

S Corporation – A tax classification known as an S corporation can shield the assets of small-business owners from double taxation. An S corporation uses pass-through taxation, which allows owners to claim a portion of business profits on their personal tax returns.

This prevents the double taxation of profits (once under the corporation and again under the owner). Since an S corp is a subchapter corporation, the “S” in S corp stands for “subchapter”. When incorporating a company, you must first create a C corp that satisfies the criteria for being classified as a S corp.

The requirements include capping ownership at 100 individuals (not entities or partnerships), limiting those owner shares to U.S. citizens only, and electing S corp status two months and fifteen days after formally organizing your business (for the status to affect the current tax year). To choose a tax classification, you must also submit IRS Form 2553 if you form an LLC.

How Should You Organize Your Business?

Fortunately, the logical progression allows for the sole proprietor to advance or stay within that classification. Keeping good records will allow you to give complete information on all tax filings, regardless of how you choose to officially form your company.

Key Points About Taxes When Starting and Running Your Business for Long-Term Success

Reduce Tax Liability

Entrepreneurs and business owners should consider all eligible expenses incurred prior to the business’s launch as capital investments that form a part of their basis in the company, when starting a new business.

Depreciation deductions are typically used by businesses to recoup costs associated with their assets. The business may write off a certain amount of start-up and organizational expenses. Over a 180-month period, they can recoup the expenses that they are currently unable to deduct. The month that the business starts conducting active trade or operating as a business marks the beginning of the recovery period.

Increase Deductions

According to the IRS, there are many tax deductions available for your business, like investigative, discovery, research and development, equipment and infrastructure costs, and more. For instance, if you operate your business from your home or use your vehicle for your business, you’ll be able to claim a tax deduction.

With a little imagination, research, and good accounting practices including automation, you’ll be able to max these out for your benefit while remaining truthful, ethical and legally compliant.

However, there are a few guidelines. As an example, only investigative costs incurred during a broad search for or initial investigation of the business are considered recoverable start-up costs for buying an active trade or business. These expenses play a role in determining whether to buy a business. A specific business’s acquisition costs are capital outlays that cannot be amortized.

LLC Startup Cost

An LLC is created by filing articles of organization, also referred to as certificates of formation or certificates of organization, with your state. Depending on your state, the cost to file the articles of organization ranges from around $50 to $500, and you can anticipate spending anywhere from $100 – $150 on average if you get an LLC and registered agent service to take care of the initial and ongoing filings every year thereafter.

Small Business Startup Costs to Keep in Mind

There are seemingly unlimited business startup costs, but the most common are:

- Incorporation of your business

- Advertising

- Website

- Inventory

- Storage / warehouse and order processing

- Business insurance

- Software for sales, payroll, compliance and record keeping

- Business license

- Renting or buying a property from which to operate

- Equipment for producing goods/services

- Office furniture and office items like computers/printers/fax machine

- Staffing

- Taxes

- Phone/Internet

- A novelty sign that says “I’m the Boss” (not optional)

A lot of those are tax deductible over the lifetime of your business through depreciation and amortization, so remember those important terms when it’s tax time.

Things to Avoid When Starting a Small Business – Why Businesses Fail

- Trying to do everything yourself. Sometimes, you have to know what needs to be done, then delegate it. While you may be a jack of all trades, the customer will benefit from your decision to leverage everyone’s expertise.

- You didn’t test demand. With no demand, there’s no one buying anything. Unstoppable, insatiable demand will often overcome inherent weaknesses in your sales offer. The best product no one needs goes unsold.

- Hiring the wrong people. There’s a lot of cultural and societal messaging out there in the media, government, and on the street. Are you adhering to current social trends, even to your own detriment? Many businesses think they’ll be seen as cool or given a pass if they just look like they’re inclusive.

- You got an aspect of the sales process wrong. Great, you found a cheap product to source from Asia. Then, you realized it takes a whole 3 – 4 weeks before the product arrives in the U.S. No customer wants to wait that long, and the product will probably show up with Chinese characters on it. Clearly you’d need to buy in wholesale with custom packaging, then deliver it from the customer’s country.

- You got the marketing wrong. You don’t have to pour tons of money into advertising. It’s best to test with small amounts every month until you gain traction. Create a long-term web presence with a fast, simple and functional website, then test out $100 – $250 in paid ads on FB or Google to see what happens.

Gaining Visibility Fast

Don’t forget about the importance of visibility for your business. For instance, you’ll want to claim your free Google Business listing and complete your profile so customers can find you on Google maps on their smartphones, as well as give your website a free boost.

Just be careful, though, because Google’s sales associates will contact you to ask you to buy ads with them. It’s not necessary. Trust me. Google Places/Business Listing ads are just something for you to consider if you’re looking to try another paid marketing option. Organic business listings with lots of 4 and 5-star reviews, positive comments and customer recommendations are the real way to get found locally.

Another visibility issue with your business, especially in modern times, is to have a large and memorable custom business storefront sign and a clean parking lot. The first impression is huge and you want to get your overall message across quickly, gaining trust and imparting confidence that the consumer’s going to get what they want. But don’t forget that signs often require a permit process.

Conclusion: Small and Medium Size Business (SMB) Startup

Making your first dollar is important. Perhaps, it’s the most important, because there’s a valuable lesson that drove that customer’s purchase which you can learn from, extrapolate, and use to expand. Let that lesson guide you and, hopefully, you’ll find riches one day.

Some people think you have to get all your forms, licenses, and paperwork 100% correct and on point immediately. This only happens in an ideal scenario, which is rare. Most of the time, it happens in steps as you discover what you need along the way.

So don’t let the formalities get in the way of your long-term vision and goals. But do get compliant to save yourself legal hassles as soon as you can, so you can focus on your business, and not the paperwork.

Frequently Asked Questions – Business Startup Checklist

The average cost to start a microbusiness is $3,000, while the average cost to start a home-based franchise is $2,000 to $5,000, according to the U.S. Small Business Administration. Receiving your business certificate of registration and forming an LLC can cost up to $150. The costs for other conventional business models could range from $35,000 to $50,000 and include commercial real estate, machinery, business insurance, and other certifications.

Plan. Track. Hire only for what you need. Know your tax deductions like writing off portions of your home as office space for work. Buy wholesale and discount. Only seek financing if you have strong, long term market demand for a product or service. Only concern yourself with more extensive regulatory compliance and certification after you’re sure you can make a sale.

The first year’s deduction phases out once your expenses reach $50,000, but you may still deduct up to $5,000 of your qualifying start-up costs. If your start-up efforts result in the establishment of an active company or business, the amount of expenses you can deduct on your tax return for the year the business starts will be the lesser of: The remaining start-up costs are written off proportionately over a 180-month period beginning with the month in which the active trade or business commences.